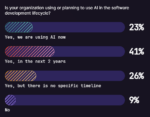

Software businesses spend a huge amount of money on research and development activities every year, spurring rapid innovation and job creation. Despite these gains, government officials worry about the continued outsourcing of research investment overseas. According to the IRS, the Research and Development (R&D) Tax Credit is one of the largest credits offered—with billions given out annually. These credits can reduce a business’s effective tax rate and increase its cash flow. The intent of the credit is to provide new funds that can be invested back into the company through new employees, technology or equipment. Many in the software industry are failing to capture the full extent of this tax credit. Due to recent regulatory and legislative changes, software developers are more eligible for the R&D credit than ever before, however, several misconceptions often deter them from applying.

MISINFORMED IDEA #1: THE R&D CREDIT CAN ONLY HELP TECH GIANTS, NOT SMALLER BUSINESSES AND START-UPS

The R&D credit is a wage-based credit, not a tax deduction. Since software companies have highly-technical and well-paid staff and contractors, the government gives them larger, dollar-for-dollar credits back. R&D credits can significantly reduce federal and state tax liability. The PATH Act of 2015 made the federal R&D credit permanent and expanded the number of eligible businesses. Before this recent legislative change, the R&D credit benefited tech behemoths but could be outside the reach of smaller companies. Government officials realized the paradox: smaller software firms that largely were responsible for innovation and job growth were not always eligible for the tax credit. Small to mid-sized businesses now can use the R&D credit to offset both regular and alternative minimum tax liability. The PATH Act also allows start-ups to use the R&D credit against payroll taxes.

MISINFORMED IDEA #2: ONLY BRAND-NEW SOFTWARE DEVELOPMENT CAN QUALIFY AS R&D

Software only needs to be new to the business, not the market, to be eligible. When many business owners hear “research and development,” the assumption can be that unless a company is developing groundbreaking application software or a new operating system, its business activities do not qualify as research and development. However, the government uses an expanded definition in which any applied sciences that solve real-world issues such as efficiency, cost and functionality qualify as R&D.

Therefore, improvements to a software program or creating a version 2.0 or 3.0 are qualified R&D activities as defined by the government. Companies that test new software or databases are engaging in R&D activities. The development of algorithms and applications, as well as network engineering and coding solutions for the implementation of a system, are qualified activities as well.

Any business that works on software for industrial purposes like control systems or other valves is also eligible for the R&D credit. Manufacturing is complex and requires various work, and there are multiple software components to industrial processes. Software affects almost every industry on a day-to-day basis. Since most work on software is technical in nature, it can count towards the credit. Every year thousands of companies claim R&D credits for a wide-ranging scope of activity.

MISINFORMED IDEA #3: SOFTWARE FOR COMMERCIAL USE IS NECESSARY TO QUALIFY FOR THE R&D CREDIT

Customizing software or developing it for use by a third-party is R&D activity regardless of whether the software will be marketed, licensed or sold. Companies with software or web developers, software consultants and other technology firms are all great candidates.

As global business operations become digitalized, businesses rely more on software companies to improve their systems and resource management tools. Designing the structural architecture, testing codes or establishing functional specification for the internal-use software of another company can also be considered R&D activity.

MISINFORMED IDEA #4: YOU CANNOT CLAIM THE R&D CREDIT IF YOU ARE BEING PAID FOR THE WORK

If a software company is being paid for its work or has a contract with the government, it may still claim the R&D credit. Eligibility for the R&D credit depends on stipulations of the contract, such as who held economic risks. Contract analysis by a tax expert is needed to understand the terms of agreement before making any claim to the credit. Treasury regulations govern exactly which kinds of contracts can qualify for the credit, but many third-party software developers claim the R&D credit each year.

The R&D tax credit is readily available for software companies. Additionally, many states offer R&D credits. Firms in the software industry have received millions of dollars from the R&D credit. The key to successfully claiming the credit is analysis by highly specialized tax professionals in your field. Reconsider how big a value the R&D credit could add to your business by further exploring this powerful incentive.